Easy Estate Planning Tips for Everyone

Aug 2, 2022

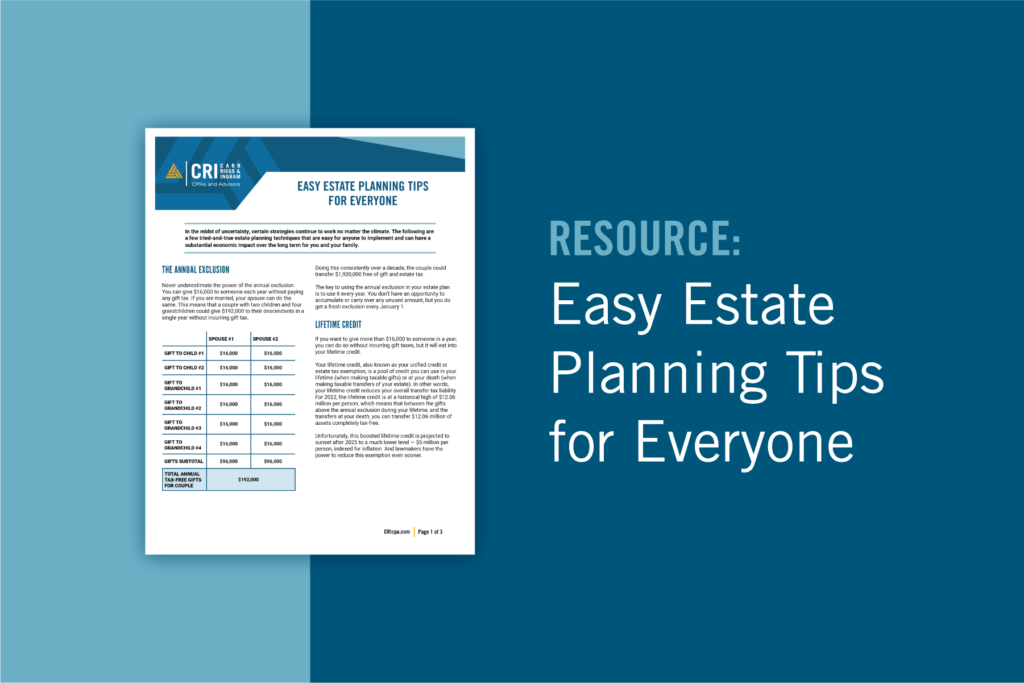

In the midst of uncertainty, certain strategies continue to work no matter the climate. Download our compilation of tried and true estate planning techniques that are easy for anyone to implement and can have a substantial economic impact over the long term for you and your family.